The job growth in the USA

(Image credit: Jack Ohman | Copyright 2016 Tribune Content Agency)

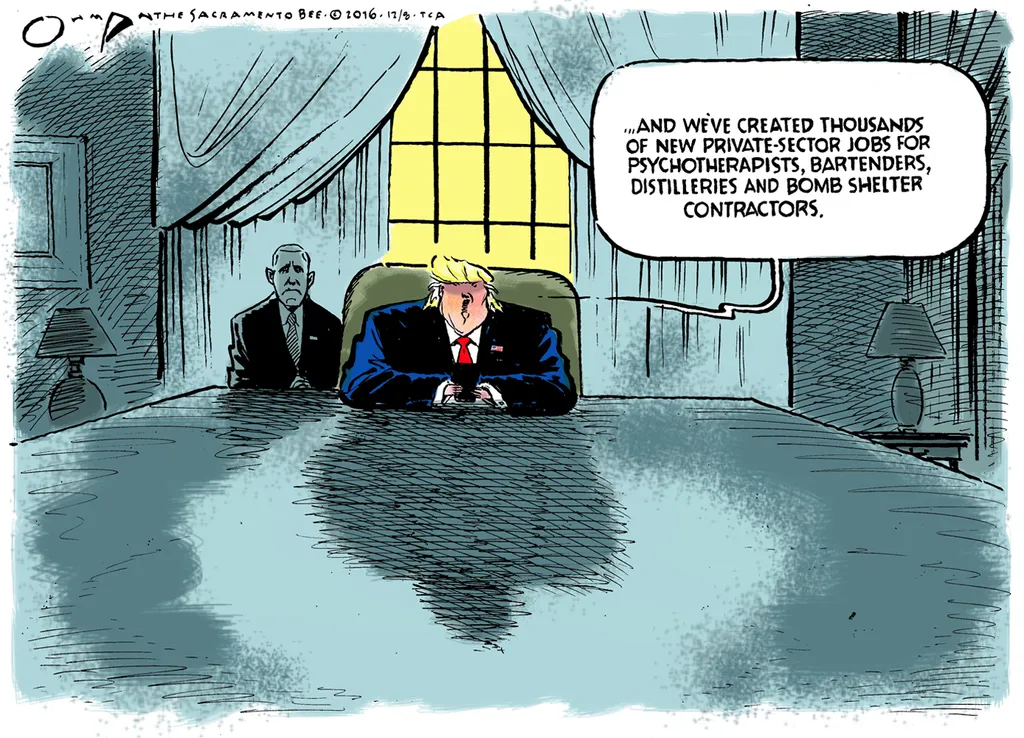

According to White House communications, 687,000 private-sector jobs have been created since Trump took office, and 100% of that job growth comes from the private sector.

But the figures:

- are not for 2025 anyway, but for a self-chosen period since he took office.

- do not indicate net job growth in the economy as a whole, because at the same time, federal employment fell by 271,000 jobs.

- deviate significantly from the official BLS totals, which show only 181,000 net jobs for 2025 as a whole.

So it's a classic trick:

➡️ selectively pick a subset of figures (private sector),

➡️ choose a favorable start date,

➡️ and ignore the rest of the economy.

What do the official figures say about 2025?

The most recent revised data from the Bureau of Labor Statistics (BLS) shows:

• Only 181,000 jobs were created in 2025 as a whole. That's 69% less than the previous estimate of 584,000 jobs. Common Dreams

• This makes 2025 the weakest year for job growth since 2020, or since 2003 outside a recession. NBC News

• Growth was almost exclusively in the healthcare sector; many other sectors stagnated or shrank. Common Dreams

• The US even lost 108,000 manufacturing jobs in 2025. Common Dreams

In short: no jobs boom, but a flat year with a few sectors that held their own.

FYI: Here you can read what the White House published about job growth. With the "normal" criticism of the Biden administration of course. Everything that's going well is thanld to Trump, everything that fails is due to the Biden administration.

A Closer Analysis

1. Big Picture: 2025 vs. Previous Years

The Bottom Line:

- 2022–2024: Millions of jobs added annually, a classic post-COVID recovery.

- 2025: After the major downward revision, the labor market turned out to be much weaker than anticipated; the BLS benchmark revision removed 911,000 jobs from the previous count through March 2025. CNBC

- From spring/summer 2025 onward, job growth has "changed little" and hovered around zero; unemployment remains around 4.2–4.3%. U.S. Bureau of Labor Statistics

Table 1 – Annual nonfarm payroll picture (schematic)

|

Year |

Approximate job growth |

Qualitative assessment |

|

|

2022 |

Several million |

Strong post‑pandemic rebound |

|

|

2023 |

A few million |

Still solid, but flattening |

|

|

2024 |

Around a couple million |

Further cooling, but still growth |

|

|

2025 |

Only a few hundred thousand after revision |

Very weak, near‑stall labor market |

This is deliberately schematic: the exact 2025 total after the major revision is low, in the order of a few hundred thousand, not the "687,000 jobs in 2025" triumph that Trump and his associates trumpet.

The BLS monthly reports for 2025 paint a consistent picture: total non-farm payrolls are virtually flat, with healthcare as the only clear positive, offset by losses in sectors including the federal government and parts of the goods-producing sector.+1

Table 2 – 2025 pattern by period and sector (direction, not exact numbers)

|

Period 2025 |

Total nonfarm payrolls |

Health care |

Federal government |

Manufacturing / goods |

|

Jan–Mar |

Small gains, later revised down |

Steady gains (tens of thousands per month) |

Flat to slightly down |

Mixed, tending weaker |

|

Apr–Jun |

“Changed little” overall |

Continues to add jobs |

Starts to show losses |

Weak, some job losses |

|

July |

Little change in total employment |

Job gain in health care |

Losses in federal government |

Little change / soft U.S. Bureau of Labor Statistics |

|

August |

+22,000 (essentially flat) |

Job gain in health care |

Losses in federal government; also mining/oil down |

Little change U.S. Bureau of Labor Statistics |

|

Sep–Dec |

Around flat on average (after revision) |

Health care still positive |

Federal roughly flat to down |

Under pressure, not a growth engine |

Key detail from August 2025:

- Total non-farm: +22,000, "changed slightly."

- Healthcare: a clear increase.

- Federal government and mining/oil: a decrease.

- The major revision (-911,000 jobs through March, particularly in leisure & hospitality, professional & business services and retail) shows that the previous monthly figures were overly optimistic—much of the "job boom" simply disappeared in retrospect.

📊 Master Table — U.S. Labor Market Pattern 2023–2025 (Qualitative Matrix)

Table A — Annual labor‑market character (qualitative)

| Year | Overall job growth | Main drivers | Overall characterization |

|---|---|---|---|

| 2023 | Strong (millions) | Broad-based: services, manufacturing rebound | Post‑pandemic normalization, still robust |

| 2024 | Moderate (millions but slowing) | Services, health care | Cooling but healthy |

| 2025 | Very weak (few hundred thousand after revision) | Health care only | Near‑stall labor market; broad weakness |

(2025 is the only year with a major downward benchmark revision, removing 911k jobs through March.)

📅 Table B — 2025 by period × sector (directional arrows)

(Based on BLS monthly releases; arrows indicate trend, not magnitude)

| 2025 Period | Total Nonfarm | Health Care | Federal Government | Manufacturing | Retail | Prof. & Business Services |

|---|---|---|---|---|---|---|

| Jan–Mar | → / ↓ (after revision) | ↑ | → | → / ↓ | ↓ (revision-heavy) | ↓ (revision-heavy) |

| Apr–Jun | → | ↑ | ↓ | ↓ | → / ↓ | → / ↓ |

| July | → (“changed little”) | ↑ | ↓ | → | → | → |

| August | → (+22k, essentially flat) | ↑ | ↓ | → | → | → |

| Sep–Dec | → | ↑ | → / ↓ | ↓ | → | → |

Interpretation:

- Health care is the only consistent growth engine in 2025.

- Federal government shows repeated losses (explicit in July & August BLS reports).

- Manufacturing is weak throughout the year.

- Retail and professional/business services were the biggest downward revisions in the benchmark update.

- Total nonfarm is basically flat all year.

🏥 Table C — Why health‑care jobs are “private” but feel public

| Dimension | Health‑care jobs (U.S.) |

|---|---|

| Statistical classification | Mostly private sector (private hospitals, clinics, nursing homes) |

| Funding sources | Large share from Medicare, Medicaid, VA, subsidies, tax credits |

| Demand drivers | Demographics + public insurance programs |

| Economic interpretation | “Market jobs on a public IV drip” — private in form, public in substance |

This is precisely why Trump communications can say “private sector job growth,” while the underlying demand is heavily government-funded.

🧩 How does ADP fit into all this?

ADP is a payroll processor that produces its own monthly estimates of private-sector job growth.

Important to understand:

ADP ≠ BLS

| Feature | ADP Private Employment Report | BLS Establishment Survey |

|---|---|---|

| Coverage | Only private sector | Private + government |

| Method | Payroll processing data + model | Large employer survey + administrative data |

| Volatility | Higher | Lower |

| Benchmarking | No annual benchmark like BLS | Annual benchmark to QCEW (hard data) |

| Usefulness | Good for direction | Gold standard for totals |

Why ADP often diverges from BLS?

- ADP measures payrolls, not employment in the statistical sense.

- ADP doesn't own a government, so if federal jobs decline (as in 2025),

- ADP appears relatively stronger.ADP doesn't have a benchmark revision like the BLS, so large corrections like the -911,000 in 2025 don't exist there.

- ADP is more sensitive to sector mix (many healthcare jobs → ADP sees growth, while BLS total growth is flat).

Bottom line

ADP may project a "private sector growth narrative" in 2025,

but that doesn't mean the economy as a whole is growing.

It simply means that private payrolls (particularly healthcare) are increasing, while government and other sectors are declining.

🧨 How does this fit into the political claims?

- If you only use ADP,

- and you choose a favorable starting date,

- and you ignore federal job losses,

- and you ignore the BLS revision,

…then you can construct a narrative like:

“700,000 private-sector jobs since Trump took office.”

But that says nothing about:

- total employment,

- net economic growth,

- or job quality.

🧩 How does Policy influence job growth?

📊 Policy Impact Matrix — U.S. Labor Market 2025

(Qualitative, based on known economic transmission channels and the 2025 BLS patterns)

Table — Sector × Policy Channel

| Sector | Tariffs | Shutdowns / Federal Disruptions | Fiscal Policy | Regulatory Shifts | Net 2025 Labor Effect |

|---|---|---|---|---|---|

| Manufacturing |

↑ Input costs, ↓ exports, supply‑chain uncertainty |

Minimal direct effect | Neutral to slightly negative |

Compliance costs | Negative |

| Construction | Higher materials costs | Federal project delays | Mixed (depends on infrastructure pipeline) |

Permitting changes | Flat / Slightly negative |

| Retail Trade | Higher import prices → margin pressure | Lower federal spending → lower demand |

Consumer sentiment sensitive |

Labor‑rule uncertainty | Negative (revision-heavy) |

| Professional & Business Services |

Client uncertainty → delayed contracts | Federal procurement delays | Sensitive to macro slowdown |

Regulatory ambiguity | Negative (revision-heavy) |

| Health Care | Tariffs irrelevant | Federal funding stable (Medicare/Medicaid) |

Strong demographic demand |

Regulatory stability | Positive (only consistent growth engine) |

| Leisure & Hospitality | Higher consumer prices → lower discretionary spending | Minimal | Sensitive to real i ncomes |

Local regulation | Negative (revision-heavy) |

| Federal Government | N/A | Hiring freezes, attrition, delayed budgets |

Direct employment cuts |

Administrative shifts | Negative (explicit in BLS reports) |

| State & Local Government | Indirect via tax revenues | Not directly affected | Budget constraints | Varies by state | Flat |

🧠 Interpretation — Why 2025 looks the way it does

1. Tariffs

- Increasing input costs → depressing margins → lower investment → fewer hires.

- Especially felt in manufacturing, retail, and business services.

2. Shutdowns / Federal Disruptions

- Direct job losses in the federal government (BLS specifically mentions this in July and August 2025).

- Indirect effect via contractors → affects professional services and construction.

3. Fiscal Stance

- No major stimulus packages → little demand boost.

- Healthcare remains stable due to Medicare/Medicaid funding.

4. Regulatory Shifts

- Uncertainty → companies postpone hiring.

- Especially in business services and manufacturing.

5. Result

- An economy that doesn't collapse, but remains in neutral, with one sector holding everything together: healthcare.

Table — Policy Scenarios and Expected Labor‑Market Effects

| Policy Scenario | Manufacturing | Construction | Retail | Prof. Services | Health Care | Government | Overall Labor Impact |

|---|---|---|---|---|---|---|---|

| Higher tariffs | ↓ (input costs, exports) | ↓ (materials) | ↓ (import prices) | ↓ (client uncertainty) | → | → | Negative |

| Lower tariffs | ↑ (cheaper inputs) | ↑ | ↑ | ↑ | → | → | Positive |

| Government shutdown / hiring freeze | → | ↓ (project delays) | ↓ (demand) | ↓ (contracting) | → | ↓ | Negative |

| Fiscal stimulus (infrastructure) | ↑ | ↑↑ | ↑ | ↑ | → | ↑ | Positive |

| Fiscal tightening | ↓ | ↓ | ↓ | ↓ | → | ↓ | Negative |

| Regulatory tightening | ↓ | ↓ | ↓ | ↓ | → | → | Negative |

| Regulatory easing | ↑ | ↑ | ↑ | ↑ | → | → | Positive |

| Health‑care funding expansion | → | → | → | → | ↑↑ | → | Sector‑specific positive |

| Immigration tightening | ↓ (labor shortages) | ↓ | ↓ | ↓ | ↓ | → | Negative |

| Immigration easing | ↑ (labor supply) | ↑ | ↑ | ↑ | ↑ | → | Positive |

Interpretation

- Tariffs are the biggest brake on 2025-like economies.

- Shutdowns primarily affect federal and contractors, but spill over into retail and services.

- Healthcare remains policy-insensitive: demographics + public funding = structural growth.

- Immigration policy is a huge labor market lever that is often underestimated.

🥃 The “2026 Early‑Year Outlook”

Table — Early 2026 Labor Market Outlook (Qualitative)

| Dimension | Outlook | Rationale |

|---|---|---|

| Total Employment | → / ↑ (modest) | Momentum from late 2025 stabilizes; no broad recession signals |

| Health Care | ↑↑ | Demographics + public funding remain strong drivers |

| Manufacturing | → / ↓ | Tariff environment still a drag; weak global demand |

| Construction | → | Dependent on interest rates and federal project pipeline |

| Retail | → | Consumer spending stabilizes but not booming |

| Professional Services | → / ↑ | Could rebound if policy uncertainty eases |

| Government (Federal) | → / ↓ | Hiring freezes and attrition continue |

| Wages | ↑ (moderate) | Labor supply improving but still tight in key sectors |

| Unemployment Rate | → | No strong upward pressure unless shocks occur |

| Risks | ↑ Tariffs, ↑ policy uncertainty | These remain the biggest headwinds |

| Upside Potential | ↑ Infrastructure, ↑ immigration | Could unlock growth in multiple sectors |

Interpretation

- 2026 starts off stable, but not spectacularly.

- No recession signs, but no broad-based growth either.

- Healthcare remains the engine.

- Manufacturing remains the brake.

- The big question for 2026: will policy continue to hold back, or will there be room for investment?

Table — Canary Sectors and What They Signal

| Sector | Why it’s a Canary | What an Upturn Means | What a Downturn Means |

|---|---|---|---|

| Professional & Business Services | Highly sensitive to corporate spending | Firms are investing again | Firms are freezing projects |

| Manufacturing (esp. durable goods) | Long supply chains, capital‑intensive | Rising orders, confidence | Falling orders, global weakness |

| Leisure & Hospitality | Pure discretionary spending | Consumers feel secure | Consumers tightening belts |

| Temp Help Services | First hired, first fired | Firms preparing to expand | Firms bracing for slowdown |

| Residential Construction | Rate‑sensitive, demand‑sensitive | Housing demand strengthening | Credit conditions tightening |

| Trucking & Logistics | Real‑time goods movement | Supply chain heating up | Demand cooling across economy |

How to read them

- If temp help + business services turn up → early expansion.

- If manufacturing + trucking weaken → early contraction.

- If leisure & hospitality drops → consumer stress.

- If residential construction rises → credit conditions easing.

Where we stand entering 2026

- Temp help: flat → no clear direction.

- Business services: weak but stabilizing → cautiously positive.

- Manufacturing: weak → brake remains..

- Leisure & hospitality: soft → consumers are cautious.

- Logistics: mixed → no strong trend.

- Housing: rate‑dependent → can pivot quickly if policy changes.